Buying a home in Malaysia is exciting, until the bank says, “Maaf, permohonan tidak berjaya.” One minute you’re already picturing where to put the sofa, the next you’re staring at a loan rejection, wondering what went wrong. Truth is, getting a property loan isn’t just about loving the house; it’s about convincing the bank you’re a safe bet, too. There are a few common slip-ups that can quietly derail your application. So before you blame bad luck, here’s a friendly, no-nonsense Malaysian guide to the Top 10 Common Reasons Property Loans Get Rejected in Malaysia and how a little prep can go a long way.

The Malaysian Property Dream: Understanding the Loan Approval Process

Getting a loan to buy property in Malaysia is a big step. It’s important to know how the loan approval process works. This process checks if you can afford the loan.

Banks in Malaysia look at your credit score to decide. They check things like:

- Credit history: A good score helps a lot.

- Income stability: Banks like steady income.

- Debt-to-income ratio: Keep this low for approval.

A good credit score shows you’re reliable with money. To keep a good score, do these:

- Pay debts on time.

- Use less than 30% of your credit limit.

- Don’t apply for too many loans or cards at once.

Showing you can pay back the loan is key. Banks need proof of your income. This includes:

- Recent pay slips.

- Income tax returns.

- Bank statements showing regular income.

Knowing these steps and preparing well can help. It’s about showing banks you’re financially stable.

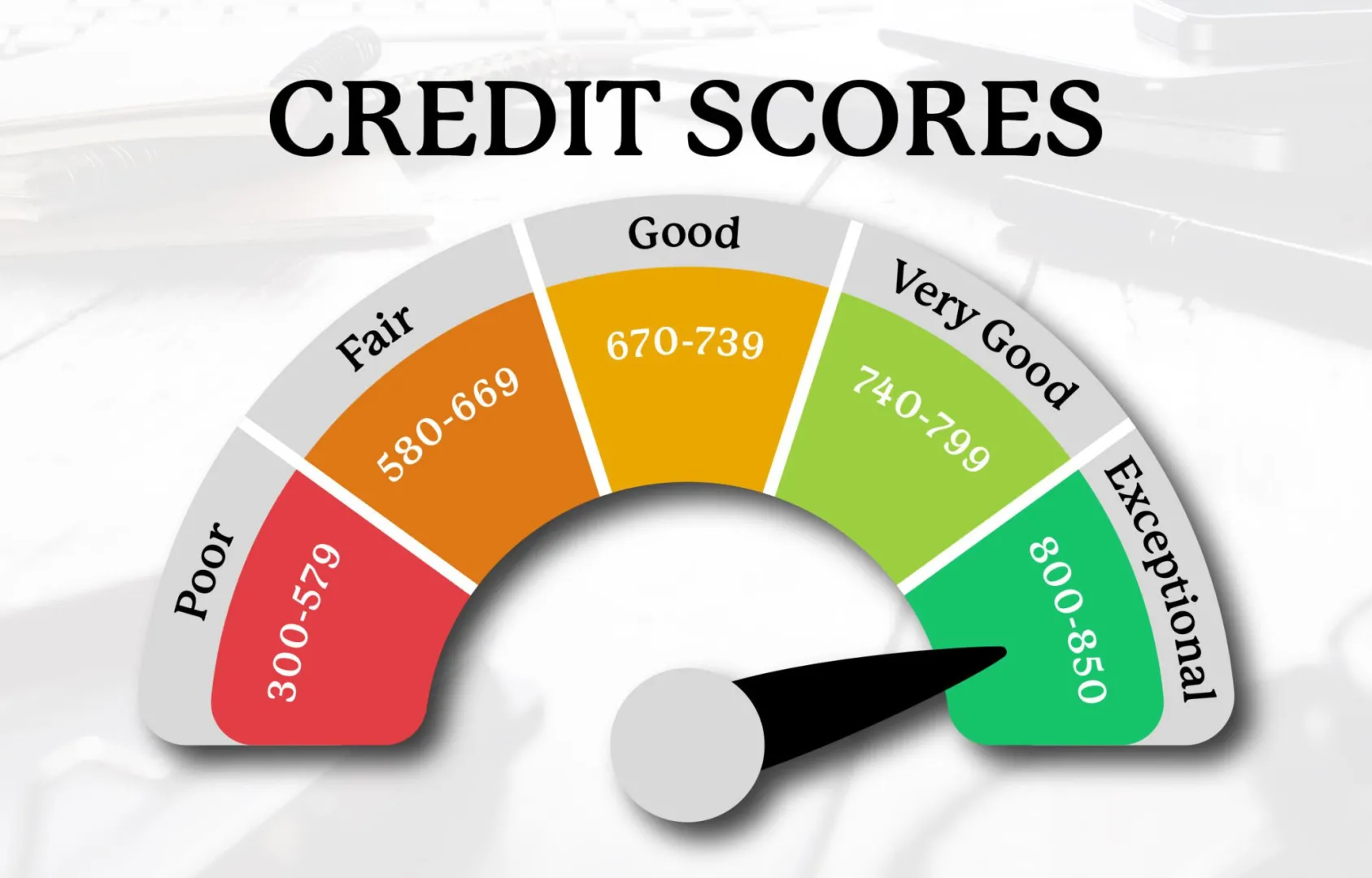

1. Poor Credit Score: When Your Financial Report Card Fails You

Your credit score is more than just a number. It shows how well you handle your money. In Malaysia, a good score can mean the difference between getting a loan and not. It’s like a financial report card, showing if you’re good with debt and credit.

A bad credit score makes it hard to get a loan. It’s based on your past with credit, how you pay back debts, and other financial matters. Lenders look at this to decide if they should lend to you.

How Credit Scores Are Calculated

Several things decide your credit score. These include how you’ve paid back loans, how much credit you use, and how long you’ve had credit. A high score means you’ve handled money well.

- Repayment history: Paying on time helps your score.

- Credit utilisation: Low balances on credit cards are good.

- Length of credit history: A longer history can raise your score.

2. Insufficient Income Documentation: The Paperwork That Makes Banks Say “Tak Boleh!”

Insufficient income documentation is a common reason for loan rejections in Malaysia. Banks need to check if you can afford to pay back the loan.

Income documentation is key in the loan application process. Malaysian banks ask for pay slips, EA forms, and commission statements to check your income. It’s important to have these documents ready and correct.

Essential Documents for Income Verification

- Pay slips for the past few months

- EA forms or other income tax documents

- Commission statements, if applicable

- Business financial statements for self-employed individuals

To avoid loan rejection, make sure you have all the needed paperwork. This includes the documents mentioned and any extra information the bank asks for.

3. High Debt-to-Income Ratio: When Your Commitments Outweigh Your Wallet

Knowing about the debt-to-income ratio is key when you apply for a property loan in Malaysia. This ratio helps lenders see if you can handle your loan and other financial duties.

The ratio is found by dividing your monthly debt payments by your monthly income. In Malaysia, lenders usually look for a ratio between 60% and 70%. For example, if you make RM10,000 a month, your debt should not be more than RM6,000 at 60%.

What Constitutes Debt Commitments?

Debt commitments are all regular payments, like car loans, personal loans, and credit card debt. Keeping a good debt-to-income ratio is important. It shows lenders you can handle your finances well.

To get a loan, manage your debts well. Pay off high-interest loans, avoid new credit checks, and have enough money for unexpected costs.

4. Property Valuation Issues: When Your Dream Home Isn’t Worth What You Think

In Malaysia, lenders look closely at property valuation when you apply for a loan. The value of your property is key. It decides how much you can borrow.

Problems with property valuation can stop your loan from being approved. Lenders use valuations to figure out the risk of lending. If the valuation is too low, they might offer less money or even say no to your loan.

Key Factors in Property Valuation

- Location: Where your property is matters a lot. Homes in the best spots are worth more.

- Property Condition: How well your property is kept, and its ag,e are important. A well-looked-after home is worth more.

- Comparable Sales: Sales of similar homes nearby also affect the value.

To avoid problems with property valuation, make sure your dream home is in good shape. Knowing the property’s value is also key. Working with trusted valuers and understanding what affects property value can help.

5. Employment Stability Concerns: The Job-Hopping Penalty

Lenders in Malaysia see job stability as key to knowing if someone can pay back a loan. A stable job is more than just a paycheck. It shows lenders that the borrower is reliable.

Switching jobs often can worry lenders. They might think the applicant’s income is shaky or they might not pay back the loan. For those who have changed jobs a lot, getting a property loan is harder.

- Lenders often want to see at least two years with the same employer.

- Staying in one job and moving up in your career can help your loan chances.

- Explaining job changes, like for better pay or job security, can ease worries.

To get a loan, showing job stability is key. This means keeping the same job for a long time or having a steady income rise.

Other Common Reasons Property Loans Get Rejected in Malaysia:

- Documentation and Legal Hiccups

- Age and Loan Tenure Mismatches

- Blacklisted Developers or Properties

- Previous Bankruptcy or Legal Issues

Conclusion: Turning Your Property Loan Dreams into Reality

Getting your property loan approved in Malaysia isn’t about luck, cable, or knowing someone “inside the bank.” It’s about preparation, clarity, and showing the bank that you’re financially steady, not financially stressed. Think of it this way: banks aren’t trying to stop you from owning a home; they just want reassurance that you can handle the commitment. Do your homework, get your finances in order, and go in prepared. With the right mindset, that “permohonan tidak berjaya” can turn into the sweetest words of all: loan approved.

Understanding why property loans get rejected is crucial to building a healthier, more transparent real estate ecosystem. Developers who proactively address affordability, documentation clarity, and financing readiness aren’t just closing deals; they’re strengthening buyer confidence and market resilience. The ASEAN Property Developers Awards (APDA) honours developers who don’t just sell properties, but make homeownership more attainable and responsible in Malaysia. Nominate now!